{kind=link}

If you’re building a custom home in BC, deposits, holdbacks, and new home warranty insurance are three different tools that protect you in three different ways. The deposit helps your project start clean, the holdback reduces lien risk in the payment chain, and warranty insurance covers certain defects after completion. If you want one accountable team to structure the contract, schedule, and documentation properly from day one, start with a custom home builder who manages the full process.

This is general information to help you plan and ask better questions. It is not legal advice. If you have a construction mortgage or a complex project, confirm payment terms, holdback handling, and warranty registration with your lawyer and lender.

At A Glance: Deposits Vs Holdbacks Vs Warranty

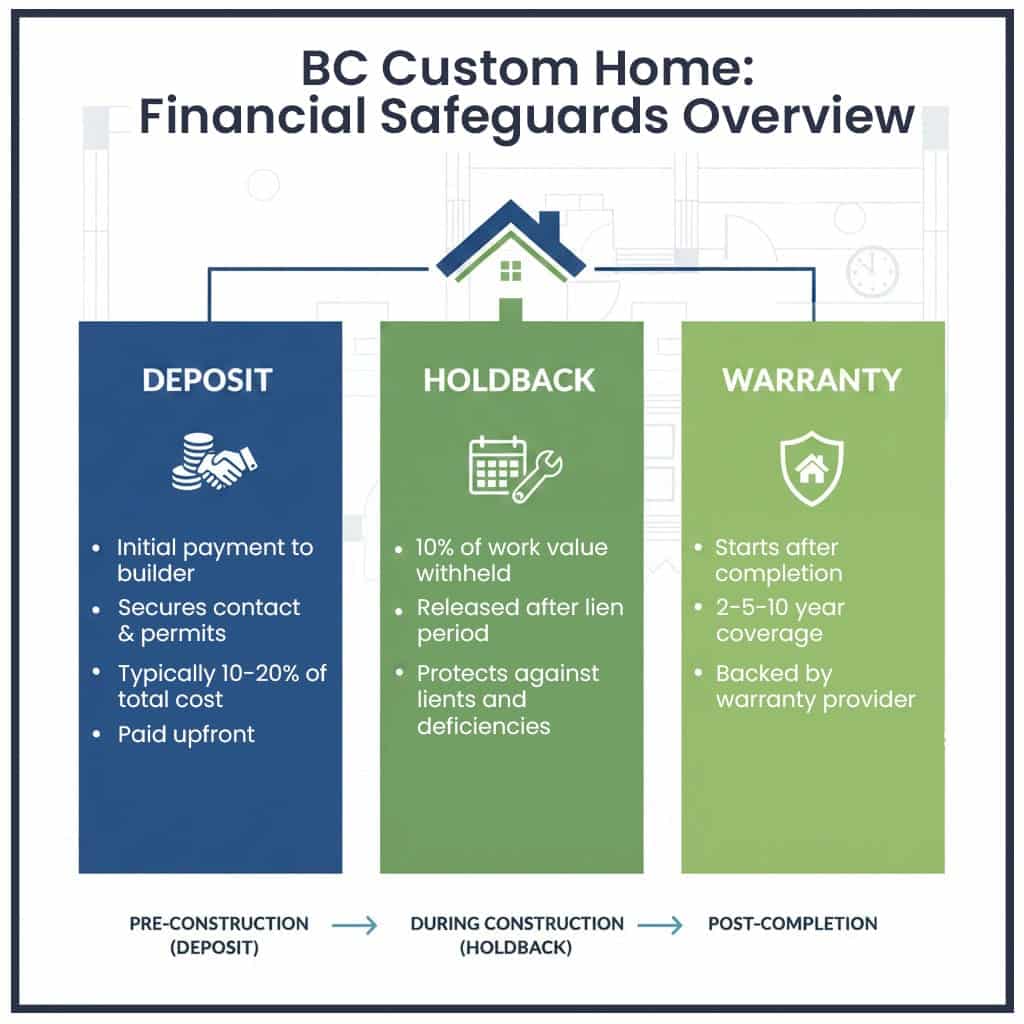

A deposit is money paid at the start of the project to secure your start date and fund early work like planning, mobilization, and long-lead purchasing (when it’s written into the contract). A deposit should always tie to clear deliverables, not vague promises.

A holdback is money you keep back from payments to reduce the risk of lien claims. In BC, holdbacks are grounded in the Builders Lien Act, which requires a 10% holdback in the situations covered by the Act.

Warranty insurance is protection that kicks in after completion. In BC, new homes built by a Licensed Residential Builder must have home warranty insurance, and BC Housing explains it protects against certain construction defects (materials and labour, building envelope, structural components).

Holdbacks In BC: What They Are And Why They Exist

A holdback is a portion of money that is not paid immediately, even when work is completed, because it helps protect the payment chain. In plain terms, it reduces the risk that you pay in full and then later discover that a subcontractor or supplier wasn’t paid and files a lien claim.

Most homeowners never think about liens until a lender brings up holdback conditions, or a contract includes holdback language. It’s worth understanding early because holdback handling impacts how your draws and final payment are structured.

What BC Law Requires At A High Level

In BC, the Builders Lien Act requires certain parties to retain a holdback equal to 10% of the greater of (a) the value of work or material actually provided and (b) the amount of any payment made on account of the contract price.

This is why you’ll often see a 10% holdback line item in construction contracts and lender draw schedules. It’s not just a “builder preference.” It’s part of how lien risk is managed under BC’s legal framework.

Who Retains The Holdback (Owner, Builder, Lender)

In practice, who retains the holdback depends on how your project is financed and how payments are administered. Owners often retain holdback amounts on payments to the prime contractor, and builders often retain holdbacks on payments to subcontractors, so the protection runs down the chain.

If you have a construction mortgage, your lender may also have a process that affects how holdback is retained and released as part of their draw administration. This is where it’s worth being conservative: you want one clear plan for holdback handling that matches your contract and your lender’s requirements.

When Holdbacks Are Typically Released (The “Holdback Period”)

Holdback release is not “whenever it feels done.” The Builders Lien Act defines key concepts like the holdback period and how it is calculated.

The homeowner-friendly rule is simple: don’t release money early just because the house looks finished. Confirm the release timing and documentation with your lawyer and lender so you don’t create unnecessary exposure.

Deposits And Progress Payments: How Custom Home Payments Usually Work

A deposit is often used to secure a place in the builder’s schedule and fund upfront work that must happen before construction moves smoothly. That can include project kickoff, preconstruction coordination, consultant scheduling, and procurement planning for long-lead items.

The deposit should also reduce chaos. When the deposit is tied to clear milestones, you and your builder both know what “start” means and what needs to be ready before work begins. This is where many projects go wrong: owners think “start” means excavation, while the builder is still waiting for final selections or approvals.

What A “Healthy” Deposit Looks Like (Structure, Not A Percentage)

In custom home building, a “good” deposit is less about a specific percentage and more about the structure behind it. You want the contract to say what the deposit funds, what documents you receive, and how changes or delays affect timing and cost.

A deposit is safer when it’s linked to tangible deliverables such as a finalized scope, an allowance schedule, a baseline schedule, and an early procurement plan. If you can’t point to what you’re buying with the deposit, it’s worth rewriting the contract language before you sign.

How To Make Deposits Safer

A practical way to reduce deposit risk is to treat it like a checklist. Before paying, confirm you have:

- A defined scope and clear exclusions

- A written change-order process

- Allowances that match your finish level

- A schedule that shows major milestones and decision deadlines

- A clear plan for long-lead items (windows, exterior doors, cabinetry, HVAC)

If you want to see what “permit-ready planning” looks like before the deposit and contract are finalized, this preconstruction overview breaks down the steps that reduce redesign and payment disputes.

Progress Draws And Payment Triggers

Most custom homes run on progress draws tied to milestones (foundation, framing, lock-up, drywall, finishing, closeout). The key is not the number of draws. The key is that payment triggers should be objective and easy to verify, with documentation that matches the schedule.

Your contract model also affects payment flow. Fixed-price contracts tend to feel more predictable for most homeowners, while cost-plus contracts often require more owner involvement in approvals and invoice review. If you’re still choosing between those models, this breakdown is a good companion read.

Home Warranty In BC: The 2-5-10 Warranty Explained

In BC, home warranty insurance is commonly referred to as 2-5-10, which generally means coverage periods that relate to (1) materials and labour, (2) the building envelope, and (3) structural components. BC Housing explains that home warranty insurance protects new homes in British Columbia against certain construction defects, including issues with materials and labour, the building envelope, and structural components.

The big mindset shift is this: warranty insurance is important, but it is not a substitute for a good process. You still want strong quality control, inspection readiness, and clear documentation during the build so problems are prevented, not just claimed later.

What Warranty Does Not Cover (And Why That Matters)

Warranty insurance does not cover every frustration that can happen in a new home. It is designed for specific construction defects, not cosmetic preferences, design changes, or normal maintenance. That matters because many disputes start when expectations are not aligned.

A smart approach is to keep two lists: deficiencies to complete before handover, and warranty items that may develop later. Your builder should make it easy to document both, track timelines, and keep communication clear.

How To Verify Warranty And Builder Licensing Before You Build

In BC, home warranty insurance is not just “nice to have.” The Homeowner Protection Act includes a mandatory home warranty requirement: a person must not build a new home unless the new home is registered for coverage by home warranty insurance provided by a warranty provider.

Before you sign, ask for the warranty provider name, the registration path for your home, and when you’ll receive the policy documents. If the answers are vague, slow down. Warranty registration should be a normal part of a professional builder’s process.

How Deposits, Holdbacks, And Warranty Fit Together

Deposits Fund Momentum; Holdbacks Reduce Payment Risk

Deposits and holdbacks can feel like they’re in conflict, but they are solving different problems. The deposit helps your project start clean and stay scheduled. The holdback reduces the risk that money flows out faster than lien risk can be cleared.

When these are structured properly, the build feels calm. When they’re structured poorly, you feel pressure at every payment because you’re unsure what you’re paying for and what you still need to protect.

Warranty Protects You After Completion

Warranty is a backstop, not a strategy. Your real protection is a builder who plans carefully, uses inspection-ready checklists, and documents decisions before work proceeds. That reduces rework, prevents delays, and limits disputes about “who said what” six months later.

If you want a broader view of what your builder should be managing across planning, construction, and closeout, this A to Z guide is a helpful reference.

Why Scope Clarity Is The Real Risk Reducer

Most payment disputes are not about math. They’re about scope. If selections are unclear, allowances are unrealistic, and change rules are fuzzy, even a fair builder and a fair client can end up frustrated.

This is why we push for preconstruction clarity. When your drawings, selections, and schedule are aligned before construction starts, deposits feel normal, draws feel predictable, and holdback handling becomes a clean process instead of a late-stage argument.

Red Flags To Watch Before You Sign

Deposit Red Flags

A deposit becomes a red flag when it is disconnected from deliverables. If the contract can’t explain what the deposit funds, or the scope is still vague, you’re taking on risk without getting clarity in return.

Other warning signs include pressure tactics, unclear cancellation terms, and deposit language that allows scope changes without clear pricing. A professional builder should welcome questions here because clarity protects both sides.

Holdback Red Flags

A big red flag is hearing “we don’t do holdbacks” without a clear explanation that matches how holdback requirements are handled in BC and how your lender expects draws to be administered.

Another warning sign is a lack of a clear plan for lien risk management. Even if everyone is acting in good faith, unclear holdback handling can create conflict right at the finish line.

Warranty Red Flags

If a builder can’t clearly explain how warranty registration works, who the warranty provider is, and when you will receive policy documents, treat that as a serious signal. In BC, warranty registration is a required part of building new homes, not a loose promise.

You also want to be cautious if “warranty” is described only as a personal guarantee with no third-party insurance structure. Even a well-meaning promise is not the same as properly registered coverage.

Questions To Ask Your Builder

Payment Terms Questions

Ask these before you pay any deposit or draw:

- What triggers each payment milestone?

- What documentation supports each draw (photos, inspection sign-offs, reports)?

- How are allowances tracked and reconciled?

- What is the change-order process, and do I approve cost and schedule impacts before work starts?

Holdback Questions

Holdback is easiest when it’s planned:

- Who retains the holdback in practice: me, the lender, or a defined holdback process?

- What is the timing for release, and what documents confirm it’s appropriate to release?

- How are holdbacks handled down the chain with subcontractors?

If you want the legal source behind holdback requirements, start with the Builders Lien Act and then confirm how it applies to your contract with your lawyer.

Warranty Questions

Warranty questions should have clean answers:

- What is the warranty provider, and when is the home registered?

- When do I receive the policy documents, and how do claims work?

- What items are deficiencies to complete before handover versus warranty items later?

BC Housing’s overview is a good starting point for understanding what home warranty insurance is meant to cover.

How Mavish Homes Keeps Payments Clear And Risk Managed

Fixed-Price Contract And Baseline Schedule

Payment clarity starts with scope clarity. Our approach is to define scope early, price the work clearly, and publish a detailed baseline schedule so you can see how decisions, procurement, inspections, and milestones connect. That makes payment triggers easier to understand and reduces midstream churn.

If you’re comparing contract models, we still recommend making the contract match your risk tolerance. Most homeowners prefer predictable outcomes, which is why a fixed-price model with strong preconstruction is often the calmer path in Metro Vancouver.

Daily Transparency Through The Client Portal

Permits, selections, and approvals create delays when communication is scattered. We use a client portal with 24/7 access, daily logs, and progress photos so you can see what’s happening and what decisions are due. When decisions are made on time, the schedule holds, and payment milestones feel earned instead of rushed.

This also helps at closeout. Clear records reduce confusion about what changed, what was approved, and what is still outstanding.

Inspection-Ready Quality Gates And Documentation

A big part of payment confidence is knowing work is inspection-ready and documented. We use internal checklists and quality gates before municipal visits to reduce rework and avoid the stop-start pattern that can inflate costs and stretch timelines.

We also plan Step Code documentation and other testing requirements early so they don’t become last-minute surprises. The goal is a smooth path to final sign-offs and a handover that feels complete.

Work With a Builder in Metro Vancouver That Offers a Stress-Free Experience

If you want a custom home builder that offers a predictable plan, we can map your payment terms to a clear schedule, manage the documentation, and keep communication tight through your build. Book a consultation and we’ll review your stage of design, your budget priorities, and how to structure deposits, draws, and holdbacks so the process stays calm.

Frequently Asked Question

What Is A Holdback In BC Construction?

A holdback is money retained from payments to help protect against lien claims and keep the payment chain safer. In BC, the Builders Lien Act requires a 10% holdback in the situations covered by the Act.

Do I Need To Keep A Holdback On My Custom Home If I’m Paying A Builder?

Often, holdback mechanics still apply, but how they are handled can vary based on your contract and whether a lender is administering draws. Treat this as a planning item, not a last-minute decision, and confirm the release process with your lawyer and lender.

When Can The Holdback Be Released In BC?

The Builders Lien Act defines the holdback period and how it is calculated, and holdback release should follow that framework. Because timing can depend on project specifics and documentation, confirm your release timing with your lawyer or lender before you release funds.

What Should A Deposit Be Tied To In A Custom Home Contract?

A deposit should tie to clear deliverables like scope finalization, allowance schedules, a baseline schedule, and a procurement plan for long-lead items. If the deposit is not linked to tangible deliverables, the contract is carrying too much ambiguity and should be tightened.

What Is 2-5-10 Home Warranty Insurance In BC?

2-5-10 is the common name for BC’s home warranty insurance coverage periods that generally relate to materials and labour, building envelope, and structural components. BC Housing explains that home warranty insurance protects new homes in BC against certain construction defects in these areas.

Does Home Warranty Cover Cosmetic Issues Or Finish Preferences?

Warranty insurance is designed to cover certain construction defects, not cosmetic preferences, design changes, or normal maintenance. Always read the policy documents you receive for the exact coverage and exclusions.

How Do I Verify My Home Will Be Registered For Warranty Coverage?

Ask for the warranty provider name, confirm the registration path for your specific home, and confirm when you’ll receive policy documents. BC’s Homeowner Protection Act includes a mandatory requirement that a person must not build a new home unless it is registered for home warranty insurance (subject to the Act’s framework and exemptions).